You just found wet floors, a dripping ceiling, or the aftermath of a burst pipe — and your first question is whether insurance will cover it. The honest answer: in many cases, yes, but the cause of the damage, your policy details, and what you do in the next hour all determine whether your claim gets paid or denied.

If you need professional water damage restoration right now, Steam Commander serves the Cypress and greater Houston area and can be on-site the same day. This article explains exactly what’s covered, what isn’t, and what protects your claim starting immediately.

Key Takeaways

- Homeowners insurance covers water damage that is sudden and accidental — burst pipes, appliance overflow, and storm-related roof leaks are typically included.

- Gradual damage, flooding from external sources, and slow leaks that went unaddressed are typically excluded.

- In Houston, mold growth can begin within 24 to 48 hours of water intrusion — delaying cleanup puts both your property and your claim at risk.

- A professional restoration company creates the itemized moisture documentation your adjuster requires; phone photos and a handwritten list do not meet that standard.

- You have the right to choose your own restoration company in Texas — you are not required to use the insurer’s preferred vendor.

Does Homeowners Insurance Cover Water Damage in Texas?

Yes. But coverage depends entirely on the cause of the damage, not the damage itself.

Texas homeowners insurance follows the industry standard: to be covered, the water damage must be sudden, accidental, and internal in origin. A burst pipe that fails overnight, a washing machine that overflows unexpectedly, or a roof leak caused by a covered storm event all typically qualify under a standard Texas homeowners policy.

What does not qualify is flooding from external sources. Rising water from bayous, street flooding, and storm surge require a separate flood policy, usually through the National Flood Insurance Program. Insurance companies in Texas apply this distinction consistently — the source of the water is the deciding factor in every claim.

Houston homeowners often assume their standard policy covers all water-related events. It does not, and that assumption costs families thousands of dollars every year.

Here is how coverage lines up under a typical Texas policy:

| Damage Cause | Typically Covered | Typically Excluded |

|---|---|---|

| Burst pipe (sudden) | Yes | — |

| Appliance overflow (accidental) | Yes | — |

| Roof leak from storm | Yes (covered peril) | — |

| Slow or gradual leak | — | Yes |

| Flooding from rain or rising water | — | Yes — separate flood policy required |

| Sewer backup | With endorsement only | Without endorsement |

| Mold from unaddressed leak | — | Yes in most cases |

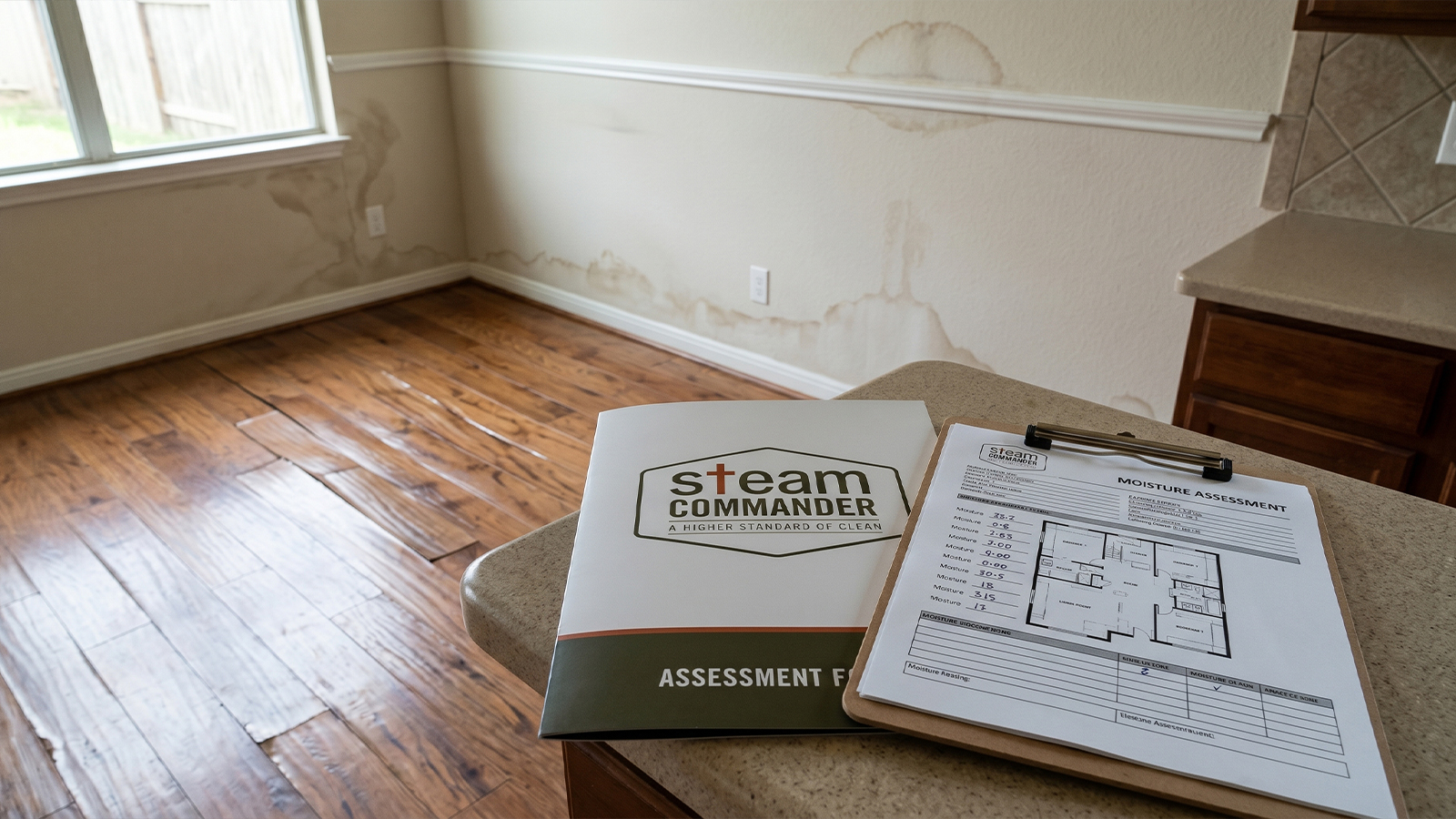

Determining the actual cause of your water damage and documenting it correctly before cleanup begins requires professional assessment. A homeowner’s best guess about the source is rarely enough for an adjuster — and being wrong can change the outcome of your claim entirely.

What Homeowners Insurance Does Not Cover — And Why It Matters

The most common reason water damage claims get denied in Texas is gradual damage. If your insurance company can argue that a leak existed for days or weeks before it was reported, they can reclassify the event as a maintenance failure rather than a covered loss. This is not a technicality. It is the standard applied to thousands of insurance claims every year.

Flooding from external sources is a categorical exclusion. Bayou overflow, neighborhood street flooding, and storm surge all require a separate flood policy — no standard homeowners insurance policy in Texas will cover them. Sewer backup is also excluded unless a specific endorsement has been added. Mold damage that results from a leak that was not promptly addressed is typically excluded as well, even if the original leak would have been covered.

What “Sudden and Accidental” Actually Means

This is the phrase that determines whether your claim succeeds or fails.

For water damage to be covered, the event must have occurred without warning and without the homeowner’s knowledge or neglect. A burst pipe that gives out overnight is a clear example of sudden and accidental damage. A pipe that has been seeping behind a wall for three weeks and finally fails is not. Insurers are trained to look for exactly that distinction — and they are good at finding it.

DIY cleanup that disturbs materials before an adjuster documents the scene gives the insurer grounds to argue the damage was pre-existing or gradual. Shop vacuums and fans do not remove moisture trapped inside walls, subfloors, or insulation. A surface that looks dry is not necessarily dry. Without thermal imaging and moisture meters, hidden saturation continues damaging structural materials long after the visible water is gone — and it stays invisible until remediation costs have already multiplied.

What About a Slow Water Leak?

Almost always excluded. The longer a leak has been present, the stronger the insurer’s argument that it was a maintenance issue rather than an accidental event. If you discovered a slow leak from a pinhole pipe, a failing supply line, or a roof that has been allowing water in gradually, document when you found it and call a restoration company immediately. Acting quickly after discovery is the only factor that can work in your favor.

Water and Mold Damage: Why Houston Homeowners Can’t Wait

Houston’s climate compresses every timeline after a water event. In a warm, humid environment like Cypress, mold growth begins within 24 to 48 hours of water intrusion — not as a worst-case scenario, but as a near-certainty when wet materials are left without professional drying equipment. Mold colonizes behind walls, inside HVAC systems, and under flooring where it stays invisible until remediation costs have already multiplied.

A roof leak or supply line failure that goes undetected even briefly can travel through wall cavities and reach structural framing and electrical systems. What appears to be a surface repair can escalate into a major structural project once saturation reaches load-bearing elements. Without a professional moisture assessment, that scope of damage stays hidden until it is far more expensive — and far harder to connect to the original covered event for insurance purposes. Steam Commander offers free on-site assessments with same-day response so the 48-hour clock does not run out before documentation is in place.

Does Insurance Cover Mold Cleanup?

Coverage exists in some Texas homeowners policies, but only when the mold is a direct result of a covered water damage event that was addressed promptly. Coverage caps are typically low — often five to ten thousand dollars under a standard policy. Mold that resulted from a gradual leak, flooding, or delayed cleanup is almost universally excluded. In Houston, the 48-hour mold window is not just about preserving your property — it is about preserving your eligibility for coverage. Once that window closes, the insurance argument shifts away from you.

How to File an Insurance Claim for Water Damage in Houston

The sequence matters as much as the steps.

After discovering water damage, stop the source if you can safely do so. Then call a certified restoration company before you call your insurer. This is how you get professional moisture documentation in hand before the adjuster sets an initial estimate. Once the restoration company has begun documenting the damage, file your insurance claim as quickly as possible — delays in reporting give the insurer grounds to question the timeline.

Your deductible applies regardless of fault, so understanding that number upfront helps you make a clear-eyed decision about proceeding. You are also entitled to choose your own restoration company; the insurer’s preferred vendor represents the insurer’s interests, not yours.

Working With Your Insurance Adjuster

The adjuster’s job is to assess your insurer’s liability. Their first estimate is frequently low and is not final.

A restoration company’s thermal imaging report, moisture meter readings, and written damage inventory give you the evidence needed to support your insurance claims and contest a low settlement. Adjusters are trained to identify signs of gradual damage — disturbed materials, cleaned surfaces, and missing documentation are all flags that can reduce or eliminate a payout.

Having a restoration company document the scene before the adjuster arrives means your claim is built on professional evidence rather than verbal description. Steam Commander provides adjuster-ready documentation as part of every on-site assessment. Call (832) 813-2175 to get that process started.

Conclusion

The difference between a covered claim and a denied one — and between a manageable cleanup and a five-figure remediation — is often decided in the first hour. Policy language is not designed to make this easy, and Houston’s 48-hour mold window leaves very little room for hesitation.

Steam Commander provides same-day response and a free on-site assessment for homeowners in Cypress and the surrounding area, including professional moisture documentation you can submit directly to your adjuster. Call (832) 813-2175 now. A certified assessment in the first hour is how you protect your property and your claim at the same time.

FAQ

Does homeowners insurance cover water damage from a burst pipe in Houston?

Yes. A burst pipe is one of the clearest examples of a sudden and accidental event that standard homeowners insurance covers. Document everything before cleanup begins and contact a restoration company to create a professional moisture assessment before the adjuster arrives.

What water damage does homeowners insurance not cover in Texas?

Gradual leaks, flooding from external sources, and sewer backup without an endorsement are the three most common exclusions. Mold cleanup resulting from unaddressed water damage is also typically excluded or subject to a low coverage cap.

How do I prove my water damage was sudden and accidental?

A certified restoration company creates timestamped moisture meter readings, thermal imaging reports, and a written damage inventory that establishes cause and scope before any cleanup disturbs the scene. This documentation is the primary evidence an adjuster uses to classify the event.

Can I choose my own water damage restoration company in Texas?

Yes. Texas homeowners are not required to use an insurer’s preferred vendor. Choosing an independent restoration company means the documentation is created to represent your interests, not the insurer’s.

How quickly does mold grow after water damage in Houston?

In Houston’s warm and humid climate, mold colonization can begin within 24 to 48 hours of water intrusion. This timeline applies year-round, which is why professional cleanup must begin immediately rather than after the claim is processed.

Will my homeowners insurance cover mold cleanup after a water leak?

Coverage for mold cleanup exists in some Texas policies when the mold is a direct result of a covered water damage event that was addressed promptly. Most policies cap this coverage at five to ten thousand dollars, and mold resulting from delayed or inadequate cleanup is almost always excluded.

What should I do before the insurance adjuster arrives for a water damage claim?

Call a certified restoration company before the adjuster visits so that professional moisture documentation is already in place. Do not disturb materials, move wet contents, or begin cleanup before the damage has been fully documented — doing so can give the insurer grounds to question the cause or scope of the damage.